Tom Cooper

Co-produced by R. Paul Drake

Considered one of our favourite holdings is EPR Properties (NYSE:EPR). In case you aren’t conversant in the corporate, we suggest that you just begin by studying our investment thesis earlier than going into this replace.

EPR is a internet lease REIT like Realty Earnings (O), Agree Realty (ADC), and Nationwide Retail Properties (NNN).

Nevertheless, as an alternative of investing in conventional internet lease properties akin to Walgreens (WBA) pharmacies or Greenback Basic (DG) comfort shops, EPR invests in experiential properties akin to film theatres, golf complexes, ski areas, and plenty of others. These properties have offered increased complete returns over very long time intervals, however they’re additionally considerably riskier and so they suffered tremendously throughout the pandemic.

EPR Properties

The massive information this month is that Cineworld (OTCPK:CNNWQ; OTCPK:CNWGQ), which owns Regal Cinemas, is submitting for chapter.

Regal is a serious tenant of EPR. EPR shares have dropped from round $55 to round $38, or about 30%.

So what ought to we do about our EPR holdings? Purchase? Promote? Maintain?

We requested our analyst R. Paul Drake to take a deep look. Right here follows his report.

The underside line on the finish is that, in the long term, it issues little what Cineworld does. Looking 5 years, EPR finally ends up with the identical earnings, or probably extra.

In each circumstances, the CAGR to truthful worth in 5 years could be above 15%. And you’d receives a commission good cash to attend.

However within the worst case, the street there might be tough.

Appears to be like Like Chapter 11 for Cineworld

There may be leisure worth within the bulletins by Regal and their proprietor Cineworld that preceded the information that they’re prone to file. They said that regardless of a gradual restoration of demand since reopening in April 2021, current admission ranges have been beneath expectations. These decrease ranges of admissions are as a result of a restricted movie slate that’s anticipated to proceed till November 2022.

What entertains me about that is that Regal administration didn’t venture revenues primarily based on a movie slate that has been well-known for a lot of months. One wonders the place they bought their expectations.

In Chapter 11 bankruptcies, the probably course right here, the bankrupt agency can reject its leases and power a renegotiation. Regal could be dumb sufficient to attempt that. The issue is that in that case the owner can simply take again the properties, and EPR in all probability would.

I coated this side at some size in a separate article referred to as EPR Properties: Those Darn Tenants Keep Paying Rent. What the pandemic led EPR to find is that lots of their theatre properties are price way more for different makes use of than they’re as theatres.

As CEO Greg Silvers put it on the Citi International Property CEO Conference:

“We offered a theater late final 12 months for industrial conversion, and other people had been asking us. So, how did they convert the constructing? They used a bulldozer…”

He additionally was requested if they’d benefit from the possibility to repossess and promote extra theatres if they may, and mentioned sure.

This makes strategic sense; EPR desires to cut back its fractional theatre publicity (now 41% of base hire). It additionally makes tactical sense; EPR proved capable of promote their theatre properties at a 6% cap fee on the Internet Working Earnings (“NOI”) they had been producing for EPR as theatres.

The properties they purchase are available in at cap charges of round eight%. This makes it accretive to shareholder worth to promote theatres and purchase one thing else.

However maybe Regal pays as little consideration to the worth of the theatre properties they lease as they apparently do to the present movie slate. We view this as unlikely however suppose Regal rejects the lease and EPR takes the theatres again.

What occurs then?

After reviewing the essential EPR enterprise mannequin and gaining some context from current historical past, we are able to take a look at a mannequin assuming that EPR repossesses all Regal theatres.

EPR Properties – A Easy Abstract

It’s price emphasizing that EPR has a stellar stability sheet and a historical past of managing it effectively. There isn’t any threat of chapter for EPR. The problems are earnings and dividends within the close to time period.

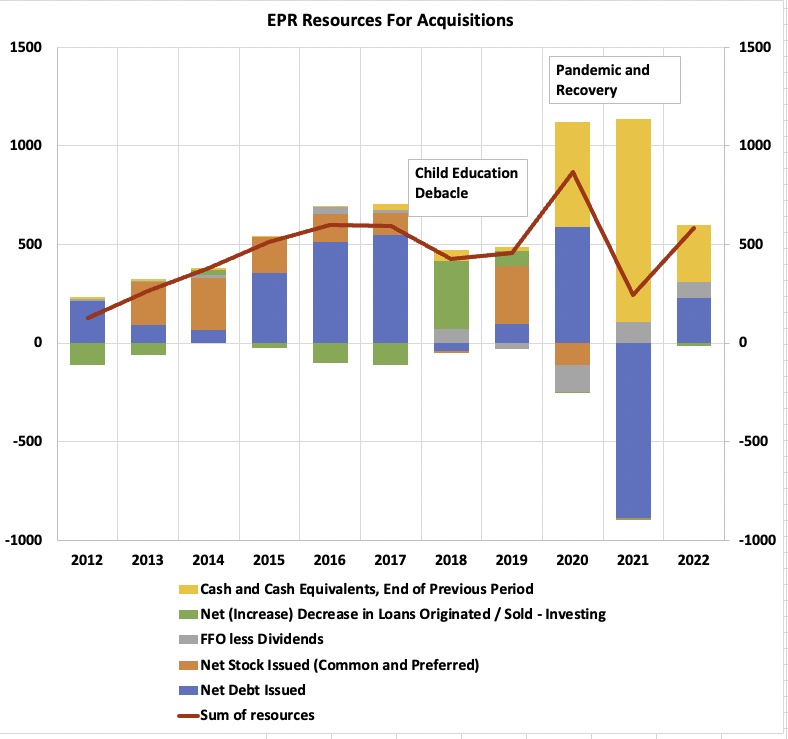

Within the REIT enterprise, what drives development is growing the quantity and worth of the properties you maintain. EPR is concentrating on annual acquisitions of $600M.

This displays a sure group of individuals doing the work to search out, underwrite, and purchase new properties. The quantity is just not simply moved, though the end result fluctuates from 12 months to 12 months.

EPR buys at a cap fee (the ratio of Internet Working Earnings, or NOI, to cost) of eight%. Their base mannequin for rising Funds From Operations, or FFO, works like this:

R. Paul Drake

Within the absence of issues, right here is how this goes for shareholders. In spherical numbers, to do $600M in internet acquisitions, EPR makes use of $250M of debt, $50M of retained earnings, and $300M of capital from share issuance. They’re and all the time have been on an exterior development mannequin.

The ballpark enhance within the share depend is between 6% and eight%, relying on inventory worth. So FFO/share ought to develop at maybe four% from acquisitions.

With a dividend that has run above 6% routinely, that pushes the anticipated complete financial return above 10%. That is what we might anticipate if Cineworld retains their present leases. Ten years in the past, the entire return was increased as a result of there was additionally ongoing a number of enlargement.

Sadly, EPR has seen considerable issues since 2017. Taking a look at these beneath supplies the context from which to construct a mannequin for the case that Cineworld rejects the lease and EPR repossesses all of the theatres they function.

The oversimplified abstract is that this: EPR would lose about $21M per quarter in NOI. In 2021, they had been capable of promote repossessed theatres at beneath a 6% cap fee on EPR’s NOI. Assuming they’ll now get 6.5%, promoting all these theatres would produce $1,292M. However the lack of that $21M per quarter would take annual NOI down about 15% first.

Shopping for new properties at an eight% cap fee would garner an NOI of about $26M per quarter, a 20% enhance on the brand new, decrease NOI. However there are two issues with this. It will not fairly make up the distinction and it will take years to come back about.

How this would possibly play out is mentioned within the subsequent few sections. Readers with much less curiosity in particulars might need to skip forward to the part entitled “Abstract and Valuation”.

Context from Historical past

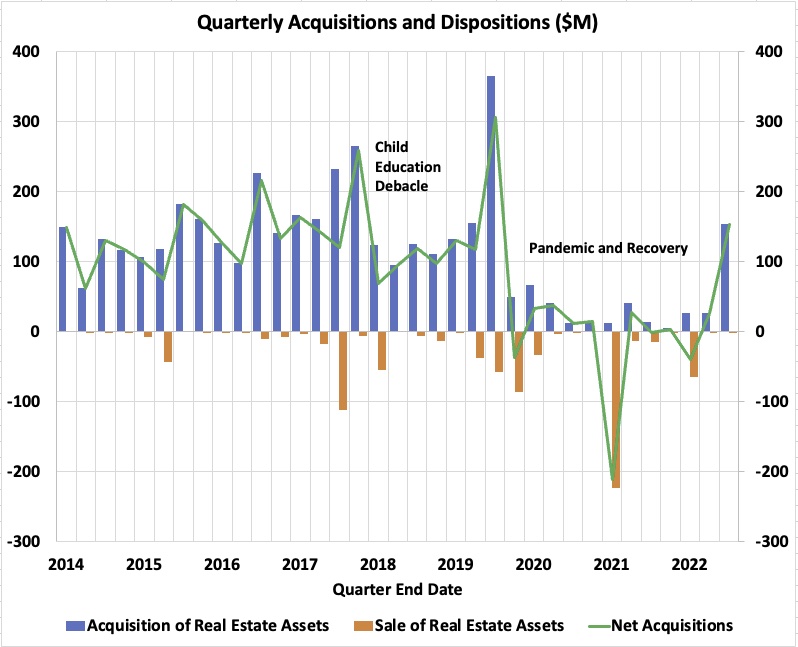

Right here is the historical past of acquisitions and inclinations for EPR, which does little redevelopment and whose growth for designated tenants is included in acquisitions:

R. Paul Drake

Within the years earlier than 2018, EPR was steadily growing its annual acquisitions, reaching a mean degree above $150M per quarter in 2017. Sadly, their foray into childhood training services proved to be a poor determination with impacts in 2018 and 2019. Then in late 2019, a serious theatre acquisition pushed their complete for that 12 months again up close to $600M.

I didn’t discover that interval simply after 2017 in depth. It’s clear that that they had main points with some mortgage loans and that this impacted their tempo of acquisitions in 2018.

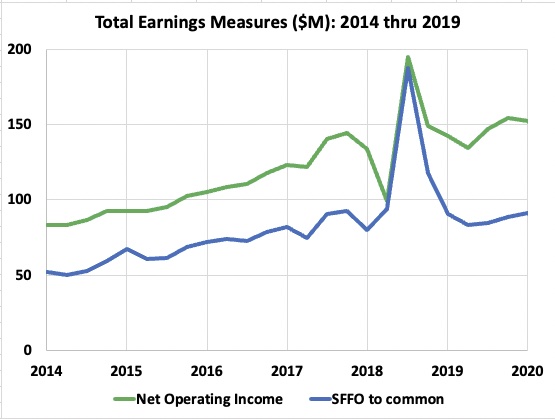

We are able to see the ends in the historical past of two parameters. These are Internet Working Earnings, or NOI, and Easy Funds From Operation, or SFFO. Right here SFFO (to frequent) is complete revenues much less property working bills, Basic & Administrative prices (“G&A”), different working bills, curiosity expense, and most well-liked inventory dividends.

R. Paul Drake

[For REIT geeks: this SFFO comes out pretty close to the NAREIT FFO. EPR also has pretty small recurring capex as is often true of net lease REITs. They also have small straight-line rent. Between these and other factors, the REITbase AFFO comes out pretty close to the SFFO. So we stick with SFFO below.]

Wanting on the graphic, what’s necessary right here is just not the lumpiness in 2018, which displays huge and non permanent modifications in mortgage earnings and different working bills. NOI and SFFO each elevated to new highs in 2019, in comparison with 2016.

It additionally issues how a REIT finds the cash to fund their internet acquisitions. The story for EPR is extra difficult than many:

R. Paul Drake

The long-term intent of EPR and most REITs is to make use of inventory issuance, retained earnings, and new debt as the primary sources of capital. This was the story from 2012 via 2017.

However as well as, EPR is within the mortgage mortgage enterprise on high of their property leases. They mortgage cash to tenants for development or different causes.

The mortgage portfolio had a stability of $970M on the finish of 2017. In 2018 EPR collected $350M from the cost of loans on ski areas and $70M from cost of different loans.

On the finish of 2021, the mortgage portfolio was all the way down to $370M (it contains no loans on theatre properties). On internet, the discount of that portfolio offered sources to help acquisitions in 2018 and 2019.

EPR entered 2020 with about $500M in money (gold bar). They supposed to make use of this to amass new properties. However then the pandemic hit.

EPR elevated their debt by greater than $650M in 2020, simply to have money in case governments compelled their tenants to remain closed for a really very long time. (This concerned a $1B draw from a credit score revolver.) They entered 2021 with about $1B in money however by the tip of the 12 months had paid down all that non permanent debt.

EPR entered 2022 with almost $300M in money and will internet about $80M in retained earnings. To satisfy their guided degree of acquisitions for the 12 months, which is $600M on the midpoint, they’ll want one other $245M. My guess is that they’ll get this by elevating extra debt, which is what the graphic exhibits.

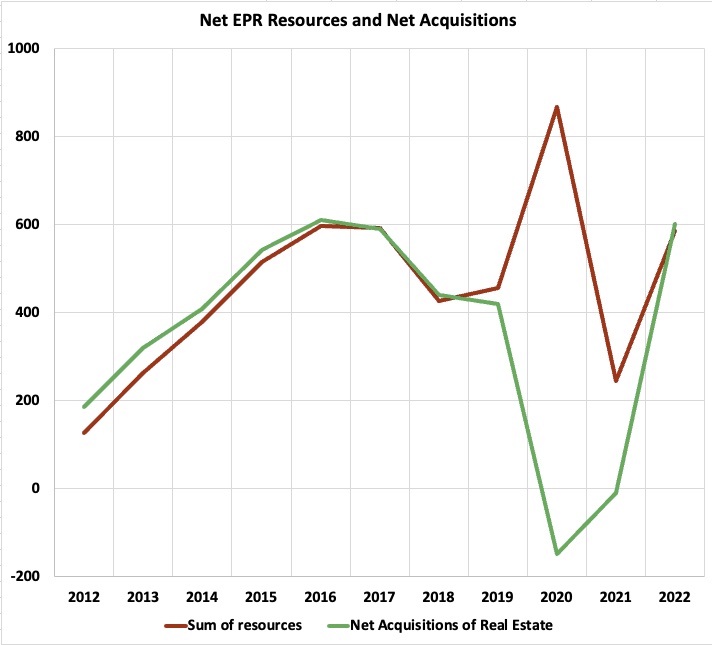

The above dialogue informs the historical past of their internet acquisitions of actual property, in comparison with the sources right here:

R. Paul Drake

We are able to see that sources and expenditures had been in shut alignment till the gyrations of the pandemic. Going ahead, EPR clearly hopes to get again to regular development like that of the years earlier than 2017 and has guided for $600M in acquisitions this 12 months on the midpoint.

However then we get the information of the Cineworld chapter, one other final consequence of the pandemic. Cineworld’s drawback is just not the viability of their theaters. Taking a look at their financials, working earnings have coated hire by greater than 3x.

Cineworld’s drawback is their debt. In the event that they and their collectors have any sense, they’ll hold the leases as they’re.

If Cineworld is wise, the present shareholders will get worn out or almost so. A bunch of collectors will get fairness, and the debt load might be a lot smaller on the opposite aspect.

However maybe the group concerned will pull a Toys-R-Us and commit monetary suicide, finally liquidating the corporate. EPR would get all 52 of its Regal theatres again. Which could occur anyway if Regal rejects the lease.

What then? Let’s look.

Mannequin Assumptions for Regal-mageddon

This part discusses particulars of my quarter-by-quarter mannequin of how this might play out. Listed below are the assumptions that make sense to me for an (virtually) worst-case mannequin of how EPR might work via these theatres.

Assume that the funds from Cineworld ($23M per quarter) go away beginning in This autumn.

Revenues would develop from earnings from these theatres, as EPR would function them till they had been offered. Assume that the rise in property working bills is balanced by these elevated revenues. This appears conservative to me.

Listed below are a number of different assumptions:

- Current rents enhance zero.5% per quarter

- G&A stays on the historic 9% of NOI

- Different opex will increase four% per quarter, far bigger than historic

- The debt will increase as wanted to help the acquisitions (see beneath).

- The common rate of interest will increase by zero.1% per 12 months. Notice that common debt maturities are lengthy.

Assume EPR would market all of the properties, although they in all probability would place a few of them with different operators. Nevertheless, concluding and shutting the gross sales takes time. Assume that the (roughly 52) properties are offered over the 4 quarters of 2024, 25% in every quarter.

At that Citi convention, Silvers famous relating to theatre gross sales that “On a money circulate foundation, we offered for a sub-six relative to the money circulate that we had been having fun with.” Assume a 6.5% cap fee, worse than EPR bought in 2021. This may present $323M per quarter throughout 2024.

My first mannequin assumed that EPR sustained their fee of $600M per 12 months in acquisitions. They’d then use the proceeds from theatre gross sales to cut back the necessity to increase money.

Nevertheless, this didn’t get FFO/share again up close to the present worth inside 5 years. EPR would need to deploy these funds ASAP, however there’s a restrict to how a lot they’ll ramp up acquisitions.

My second mannequin, with outcomes proven beneath, assumes that they handle to push acquisitions as much as $850M in 2024 via 2026.

All of the assumptions above appear conservative to me, besides the goal for acquisitions. However to no matter extent they place these theatres with different operators for related hire the necessity to push acquisitions up would drop.

There should be a good bit of that. Bear in mind, overlaying hire is just not the problem for these theatres.

The Influence on Earnings

The earnings enhance for the case when Regal doesn’t reject the leases was mentioned earlier. Now think about earnings for the case with repossession of all of the theatres, adopted by their sale based on the assumptions simply detailed.

To make the calculation easy, I assumed that EPR first paid down debt utilizing the proportion of the proceeds equal to the unique debt issuance (40% of the property worth as a theatre). Then they tackle new debt when shopping for the brand new properties. That is an apparent oversimplification however mustn’t make a distinction on internet.

This subsequent graphic exhibits one solution to have that play out within the sources for acquisitions.

R. Paul Drake

Within the absence of the theatre gross sales, yearly would appear like 2023 and 2027. The diminished share issuance happens when additional cash is out there.

Nevertheless, the profit is lower than one would possibly hope. For a share worth of $50 to $70, the distinction in complete shares issued is barely 5 to 7M out of about 100M in 2027.

Abstract and EPR Inventory Valuation

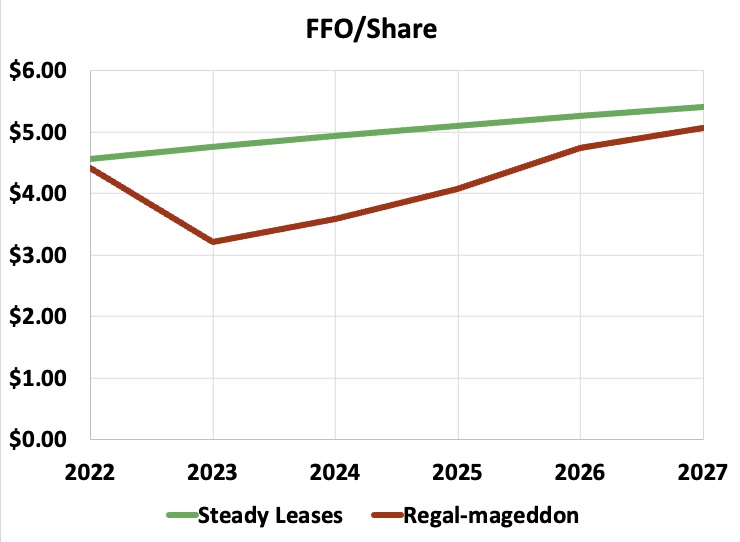

Evaluating the 2 circumstances, one with regular leases and the opposite the place EPR will get again all of the theatres, here’s what occurs to FFO/share.

R. Paul Drake

FFO/share would drop to barely beneath the current dividend in 2023 if the theatres had been all repossessed and offered as modeled. After that, it will climb extra quickly, reaching almost the worth obtained within the case the leases are regular.

All however one of many assumptions above are pessimistic. EPR would handle to rapidly place among the theatres with new operators. In different methods, their earnings could be bigger too.

My expectation could be that FFO/share wouldn’t drop as a lot as proven and would get better to increased degree than seen right here. However the optimistic assumption that’s essential to make that true is for EPR to ramp up their acquisitions to unprecedented ranges for a number of years.

The results of this story has two components. Considered one of them is that EPR might get better from the repossession of all of the Regal cinemas, adopted by their sale. However this may take a number of years. They haven’t but completed closing the sale of the final of the eight theatres they bought again in 2020.

As to valuation, on the present $38 worth, the present FFO/share a number of is eight.5. That’s simply too low. It will worth no long-term development fee on this 12 months’s FFO/share.

However no person ought to mistake EPR for a REIT that deserves a 20x a number of, both. They can not develop quick sufficient.

Assume development of earnings per share at a fee close to three.1%, roughly consultant of the bottom case above. Taking the expansion to be indefinite, and making use of a 10% low cost fee, one will get an earnings a number of of 15x.

Multiplying the guided 2022 FFO/share of $four.47 instances 15 provides you a share worth of $67, related to the regular lease case. This may go up as FFO/share will increase going ahead, reaching $81 in 2027.

Within the Regal-mageddon case, the FFO/sh in 5 years is available in $5.07. This might indicate a $76 worth. The end result for each these circumstances is that the mixture of FFO/share development and a dividend of eight.6% ought to generate a complete return effectively above 15% over the following 5 years.

However issues additionally might go worse. And the value might take a superb whereas to maneuver a lot. The market hates uncertainty, and uncertainty has positively gone up with the announcement from Regal.

Takeaways

My conclusion is that EPR mustn’t settle for a punishing lease renegotiation from Regal and Cineworld. If that’s what these events need, simply take again the theatres.

Maybe extra probably, within the occasion of lease rejection, could be that EPR calls for both the identical hire or takes the property. This might produce a case intermediate between these mentioned above.

Your complete saga of EPR illustrates the draw back of investing in properties at excessive cap charges. They’re that costly for good causes.

Issues can and typically do go fallacious. This hurts returns.

That’s the reason the market costs such REITs at a excessive dividend yield. At its present fee of $three.30, the EPR dividend nonetheless has 36% to go to return to its 2019 degree of $four.50.

Seeing this any time quickly seems to be unlikely to me. On any path, it seems to be like EPR will take about 5 years to push FFO/share to $5. The dividend for 85% of that will be $four.25.

My backside line is that by holding EPR you’ll do effectively inside 5 years, and maybe sooner. You additionally receives a commission very effectively to attend.

What you select to do with EPR might mirror your individual context. One finally expects giant positive factors. EPR is a tremendous holding for our Core portfolio. A Core-Portfolio investor, probably youthful, with a time scale giant in comparison with 5 years, might fairly sensibly hold accumulating (and particularly if the value retains dropping). Paul, as a retired investor, prefers positions that appear extra prone to produce positive factors sooner. However promoting at a loss wouldn’t make sense. There aren’t any grounds for desperation.

{kind=link}